Picking up a brand-new car is exciting, and part of the process includes the salesman explaining a number of other options that you may or may not need.

One of them will be GAP insurance, and in the excitement, it’s easy to buy what’s being offered without doing some research and looking at other prices.

You may have just set up a hefty finance arrangement and might not want to pay another sum of money towards GAP insurance. But then there’s the advantages of having it… What will happen if a year down the line you’re in an accident and your car gets written off?

In this article we look at some of the facts to help you decide.

Vehicle depreciation

It’s well known that your vehicle starts depreciating rapidly as soon as you drive it off the forecourt. Depreciation is a driver’s biggest cost after fuel purchase and with 10,000 miles a year on the clock, the average car will have lost around 60% of its value by the end of its third year, according to the AA.

So what exactly is GAP insurance?

It stands for Guaranteed Asset Protection (GAP). It’s the difference between the amount you paid for your car, or owe on your finance, and the amount your insurance company will give you if it is written off or stolen.

The crunch comes when you claim on your vehicle insurance after an accident or theft and realise that the amount you will be paid out is a lot less than the original amount you paid for it.

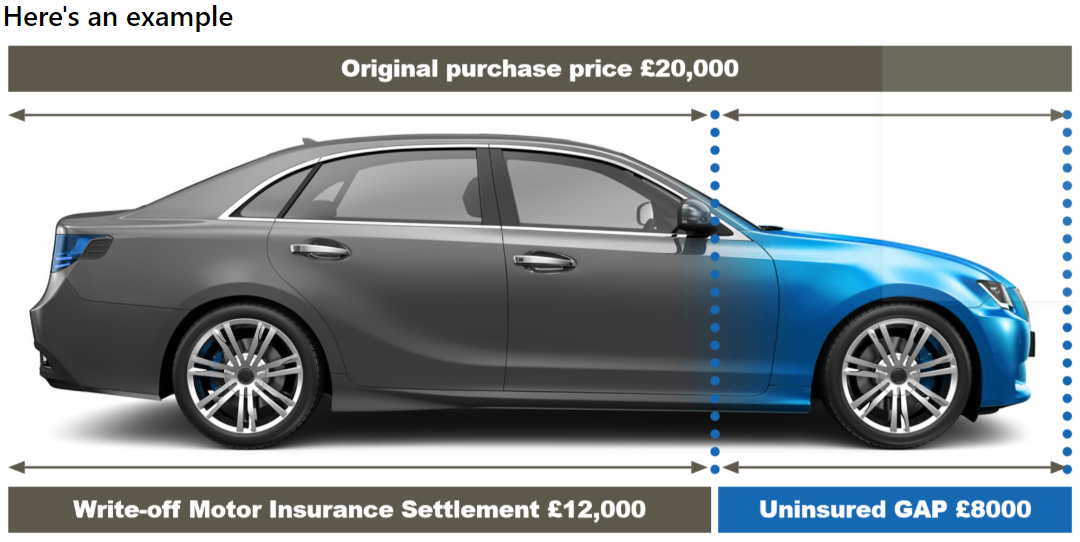

For example, if your car is just 18 months old and you’d paid £20,000 for it, your car insurer will only pay out what it’s now worth – for example £12,000.

So although you could buy another similar car that’s 18 months old you may want to replace it with a brand new one.

This is known as Return to Invoice, or Back to Invoice GAP insurance and useful if you’ve paid cash for the vehicle.

Once the claim is settled your GAP insurance will pay out the difference between the pay out from your car insurer and the cost of a replacement vehicle matching the original model’s specification.

GAP insurance can only be purchased if you have a comprehensive motor insurance policy.

What if I owe money on finance?

If your car is written off or stolen you may find yourself in a panic as you’re still paying a monthly amount to a finance company and there could be years left before the whole loan is paid off.

This is when GAP insurance is a prudent option to give you reassurance that the shortfall is covered.

To pay off your outstanding finance loan GAP insurance will pay the difference between what the insurance company pays you on your total loss claim, and what is left to be paid.

When doing your research you may see policies called ‘Finance GAP’ or ‘Vehicle Replacement GAP’ – read the descriptions carefully and make sure everything is covered, so you can quickly and easily pay off the outstanding amount.

Remember to check the length of the policy when you buy it as you will need to take the GAP insurance out for the same length of time as your finance agreement.

Is there a lower cost way of buying GAP insurance?

In your enthusiasm it’s easy to tick the option boxes including GAP insurance at the dealership. But there may be ways to spend your money more wisely and get better value for money.

GAP insurance can often be bought more cheaply online as a standalone product. Insurance brokers sell it with clear explanations of the terms and conditions, so you can read through it at your leisure and make an informed decision.

You can shop around, just like you did when you bought your car insurance. But bear in mind some of the key factors to look out for:

- When does the policy start and stop?

- Does it pay out for your car insurance excess?

- Is the claim procedure straightforward?

- Are there any significant exclusions?

- Is there cover if another driver on your insurance policy is driving your car?

- Can you cancel the policy if you no longer need it?

Ultimately the aim is to get back on the road if the worst happens with a replacement car and any outstanding finance paid off.

Four key takeaways from this article:

- GAP insurance will pay the outstanding amount on a car loan in the event of your car being declared a total loss or stolen.

- Shop around for standalone GAP insurance policies before buying from a car dealership.

- There are different types of GAP insurance. Be sure to pick the right one for you.

- If you paid cash for your car and have taken out RTI GAP insurance you can buy the same car again.

For high quality, affordable GAP insurance visit www. https://bestpricefs.co.uk/gap-insurance-cover/ and get a quote today.